You’ve probably heard warnings in the past about adjustable-rate mortgages (ARMs). Haunted by the memory of the 2008 housing crash, many buyers see ARMs as risky, unpredictable, and best avoided.

But with today’s stubbornly high interest rates, more people are asking: could a 5/1 ARM actually work to my advantage?

It’s possible.

ARM loans today are structured differently from those before the Great Recession. For the right borrower, a 5/1 ARM can be a smart tool to save money or make your homeownership dreams come true.

Of course, ARMs aren’t for everyone. Like any loan, they have risks, and it’s important to understand how they work before signing on. This article breaks down what you need to know about 5/1 ARMs, who they’re best for, and how to decide if one fits your financial plan.

What is a 5/1 ARM loan?

An adjustable-rate mortgage (ARM) is a loan where the interest rate isn’t fixed for the entire term. "The difference between it and a fixed-rate loan is that the rate is only locked in for a certain amount of time — usually, 3, 5, 7, or 10 years," explains Rebecca Richardson, a loan officer at The Mortgage Mentor in Charlotte, NC.

“After the fixed period, the loan’s rate will change according to the index the loan is based on (usually the SOFR index) and the other particulars of the loan, like how frequently it can change and caps on how high it can go,” says Richardson.

With a 5/1 ARM, your rate is fixed for five years, then adjusts annually. With another ARM, you may have a fixed rate for 3 or 7 years, with adjustments every 6 months after that.

Important ARM terms to know

Here are the most important ARM terms to know to understand the basics of your loan.

| Term | What it means | What else to know |

|---|---|---|

| Introductory (or teaser) rate | The initial period when your interest rate is fixed—typically 3, 5, 7, or 10 years. | During this time, your rate and payment won’t change. After it ends, the loan becomes adjustable. |

| Adjustment interval | How often your interest rate changes after the fixed period—commonly every six months or one year. | Watch your loan’s index rate a couple of months before adjustments to prepare your budget for payment changes. |

| Index | The benchmark rate your ARM follows after the fixed period. | SOFR is the most common, but others like COFI may be used. Ask what index your lender uses and check the index’s historical performance before signing. |

| Margin | The fixed percentage the lender adds to the index to set your new rate. | Usually 2%-3.5%. Ex: If the index is 4% and the margin is 2.5%, your new rate would be 6.5%. |

| Initial adjustment cap | The maximum your rate can increase at the first adjustment. | Often 2% or 5%[1] |

| Periodic rate cap | The maximum your rate can increase at future adjustments. | Typically 1%-2% per adjustment period. |

| Lifetime cap | The highest your rate can ever go. | Often capped at 5% above your starting rate. |

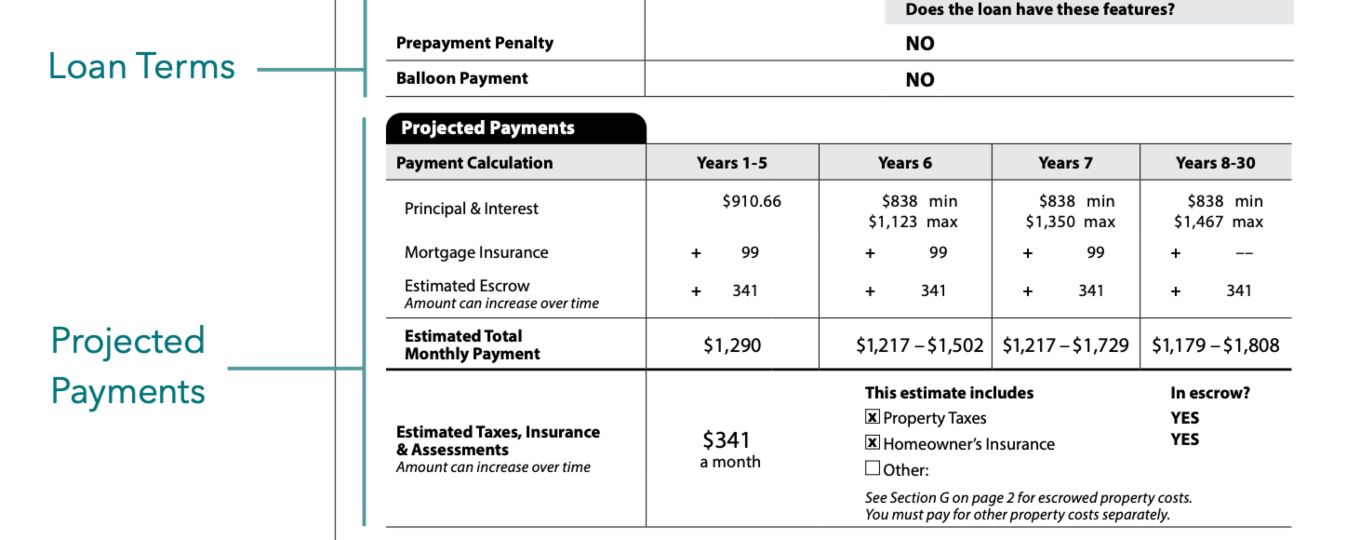

5/1 ARM loan example and calculator

Say you’re looking to buy a home for $450,000, and will put down $90,000 (20%) and finance the other $360,000. Fixed rates are at about 6.5%, but you’re considering a 5/1 ARM with a 5.46% starting interest rate (the national average ARM rate as of this writing) and 2/2/5 adjustment caps.[2]

Here’s the most you would pay under this loan, not including taxes or insurance:

| Year | Interest rate at caps | Est. monthly payment* |

|---|---|---|

| Years 1–5 | Intro fixed rate (no adjustment) | $2,035 |

| Year 6 | 7.46% (initial adjustment cap) | $2,450 |

| Year 7 | 9.46% (next periodic cap) | $2,886 |

| Year 8+ | 10.46% (lifetime cap) | $3,109 |

In an absolute worst-case scenario, you could reach your lifetime rate cap of 10.46% just eight years into your mortgage with a monthly payment of $3,109. That totals over $684,000 in interest over the life of the loan—about $225,000 more than if you had taken out a fixed-rate 30-year loan at 6.5%.

By comparison, your fixed rate payment would be locked in at $2,275, or around $834 less than your highest possible monthly ARM payment.

However, Adam Smith, a mortgage broker with The Colorado Real Estate Finance Group, notes that he’s never seen a borrower reach the lifetime cap in his decades of originating ARMs and that most ARMs today include safeguards to keep rate adjustments from spiraling out of control.

Still, he cautions that it’s impossible to predict where indices will be in 3-10 years. You could end up near your cap rate, so it’s critical to ensure you can afford that payment if it happens. Smith encourages people to study the history of the loan’s index, potential future economic data that could impact it, and the floors and ceilings associated with any ARM.

Adjustable Rate Mortgage Calculator

Estimate your ARM payments, see how rate adjustments affect your costs over time, and explore the full amortization schedule.

When a 5-year ARM can be a good idea

The key to making an adjustable-rate mortgage work is having both a realistic exit strategy and the financial flexibility to handle higher payments if your plans change.

Smith says these loans can be an especially good idea if “you know you’re only going to own your home for a brief period and want to simply take advantage of a lower rate and payment between the time you purchase and the time you sell.”

Or, "if it’s a more permanent home, you might be using an ARM to keep your payments down while the market seems to be improving, both rates and values, with the intent of refinancing it when your loan begins to adjust,” says Smith.

Let’s take a closer look at when a 5/1 ARM loan might be a good idea.

You have a clear exit plan

“If you anticipate only having the mortgage for a certain number of years, it may be advantageous to opt for an ARM and save money,” says Richardson. “As an example, if you expect to move in three years, choosing a 5yr ARM may provide a lower payment along with a few years’ buffer before the rate change would occur.”

Another example might be if you intend to fix and flip the property, which would allow you to improve the value and cash out or refinance with an improved equity position before the interest rate adjusts higher.

You have plenty of wiggle room in your budget

A 5/1 ARM can also make sense if you can afford to put in more than the monthly payment.

You could aggressively pay down the principal while your rate is low, or put money towards other investments, and then refinance into a fixed rate loan with a smaller balance at the end of your initial rate period.

For one Reddit user, that strategy worked out well:[3]

I took an ARM in 2023 at 5.75% instead of a 7.8%. Then I just refi to another ARM at 4.875% in December. I think people just fear the unknown. I’ve saved thousands compared to others who would just pay the 7.8%. And I’ll continue saving thousands more. I can save for retirement and my kids' future rather than tossing it in the fire via interest.

You expect your income to rise soon

Similarly, if you expect a significant income increase soon, a 5/1 ARM would allow you to take advantage of a lower rate upfront and then adapt to the higher rate adjustment once your salary improves. This could apply if you’re finishing medical residency, poised for a promotion, or launching a growing business.

Alternatively, you could refinance into a fixed-rate loan with a smaller loan balance, or tap into equity if you’ve increased the property’s value.

Potential risks with a 5/1 ARM loan

While a 5/1 ARM can offer meaningful savings, there are real risks, including higher payments after adjustments, refinancing challenges, and the temptation to buy more house than you can truly afford.

ARM interest rates can go up abruptly

The main risk of an ARM is that your interest rate can go up as much as 2% at a time. “Taking a 5% rate today with the possibility of it eventually being 10% is certainly a gamble in my mind,” says Smith.

With a fixed-rate mortgage, you can often pay points (i.e., extra fees) upfront to "buy down" your interest rate. One point costs the same as 1% of your loan, and can reduce your rate by about 0.25% — although this varies by lender and market conditions.[4]

However, paying points to lower your 5/1 ARM’s rate may not be worthwhile—the discounted rate often applies only to the introductory period, not to the full loan term.[5]

The difference between a variable and fixed rate isn't always worth it

As of this article's writing, the difference between the adjustable and fixed mortgage rate is 0.63% — so a 5/1 ARM may not produce as dramatic a savings as you'd expect.[6]

“Historically, ARMs had much lower rates. Now...the gap between the rates is smaller. And usually, the shorter the ARM, the lower the rate,” says Smith.

Given the smaller gap, the upfront savings may not be worth the added uncertainty without a clear idea of how you intend to use the short-term savings.

Plans change

Even if you do have clear plans, unexpected events may cause you to change them. For example, you may be planning to move to a larger house in a few years but find yourself priced out of the market or unable to afford a new mortgage at current rate.

Or, you might have been counting on a career move, but have trouble landing a job at the salary you would need to make your next real estate move.

Don’t count on rates being lower after your introductory period, and be certain you can afford the maximum possible payment, just in case.

Refinancing to a lower rate may not be an option

“Never buy on the assumption you can refi later, cautions a Reddit user.[7] "You never know where rates will be or where you will be.” If rates rise, home values fall, or your circumstances change, refinancing might not be an option.

“People who took out ARMs in 2022, when rates peaked, likely [saw] them adjust down on 3 year ARMs last year” explains Smith. “Taking out an ARM mortgage now, it’s very difficult to say what those indices will do in the next 3-10 years…Depending on the terms, you might see a two-point change the first year, a one-point change the next year, and the next, with a lifetime cap of five points."

Questions to answer before choosing a 5/1 ARM

Given the risks entailed in taking out an adjustable rate mortgage, it's important to be confident in your ability to answer the following questions:

- Can I afford the worst-case scenario if I can’t refinance or move in five years?

- Do I have a realistic backup plan?

- Could I still potentially qualify for a new loan if my income or credit took a hit?

A strong answer sounds like: “Yes, even at the maximum rate, we can comfortably afford the payment without disrupting our long-term financial goals.”

A risky one sounds like: “We’ll refinance before it adjusts” (without a concrete plan) or “Rates should be lower by then.” Five years can pass quickly. Your mortgage won’t wait if your plans stall.

The bottom line is that you should never use a lower initial monthly payment as a reason to take on a higher mortgage than you can actually afford with a fixed rate — especially if betting on rates going down.

“Lots of financially sophisticated buyers choose ARMs," observed a Reddit user.[7] "People get into trouble when they use them to buy more house than they can afford—not because ARMs are inherently bad.”

How do you qualify for a 5/1 ARM loan?

To qualify for a 5/1 ARM, lenders review factors such as your:

- Credit score: Commonly 620+ needed for conventional ARM loans; 500-580 for FHA ARM loans[8]

- Down payment: Usually at least 5% down for a conventional ARM and 3.5% for an FHA ARM[9]

- Debt-to-income ratio (DTI): Typically 45% or less needed[10]

Lenders also consider your employment, savings, and broader financial profile when determining your eligibility. They usually qualify you based on the maximum rate at the first adjustment.[11]

Questions to ask your lender

“There are so many terms to consider on an ARM,” notes Smith. “The length of the fixed period, the index and margin, the floor and ceiling, and the adjustment caps. And they can vary wildly from loan to loan. You might have a 5/1 ARM that has 2/2/5 caps. Or you might have a 10/6 ARM with 1/1/6 caps.”

Before deciding on a specific ARM loan, Smith advises people talk to a professional mortgage broker familiar with ARM loans. “Make sure they understand your short and long-term goals for your loan and your home, and work together to craft the perfect ARM for your situation.”

Once you know which ARM loan is best for your goals, clarify the fine print by asking:[12]

- What’s the highest monthly payment you could see on your loan?

- What’s the date of the first and subsequent rate adjustments, and their maximum interest rate increases?

- What’s the maximum possible interest rate on the loan?

- Does the loan have a floor (minimum) interest rate, in case rates decrease?

- Does my monthly payment recalculate when there’s a rate adjustment?

- Can my loan balance increase if my monthly payment doesn’t fully cover the interest portion?

- What index does my loan use? Where can I track it?

- Are there prepayment penalties?

- Is there an option to convert my ARM into a fixed-rate mortgage in the future? What could the new terms be?

Most of the answers to these questions should be in your loan estimate or your truth-in-lending disclosure. However, these documents can be complicated—especially for ARMs—so don't hesitate to have your lender walk you through the fine print.

5/1 ARM vs. other ARM types

The 5/1 ARM is just one of many possibilities for ARMs, which also include:[13]

- Hybrid ARMs: 5/1 ARMs are hybrid ARMs. There are different fixed-rate and adjustment periods available, such as 3/1 or 7/6.

- Interest-only (I-O) ARMs: Interest-only ARMs allow you to pay only the interest portion of your loan for a certain number of years, often referred to as the I-O period.

- Payment-option ARMs: These were more common before the Great Recession — and are often cited as contributing to the crisis — but some lenders may still offer them.[14] They allow you to choose different types of payment options each month, such as an interest-only payment or a minimum payment.

The best ARM for you depends on your comfort with uncertainty, plans to move or refinance, and expected income changes in the coming years.

If you’re risk-averse, a 10/1 ARM could make sense. It gives you a longer period of fixed rates, providing more flexibility if your plans shift unexpectedly.

But if you’re buying an investment property to renovate and sell within 18-30 months, a 3/1 ARM may be the best fit.

Bottom line: Is a 5/1 ARM right for you?

A 5/1 ARM can be a smart choice if it’s part of a concrete, realistic plan to refinance or move shortly before or after the initial fixed period ends. It can provide meaningful savings compared to a conventional loan.

✅ You might be a good candidate for a 5/1 ARM loan if:

- You have a concrete reason to sell in 5 years (or less)

- You can afford the worst-case scenario

- You're using a 5/1 loan as part of a specific strategy, like a fix-and-flip

- Your introductory rate is significantly lower than you'd get with a conventional loan, making the added uncertainty worthwhile

❌ You may want to explore options outside a 5/1 ARM if:

- You’re using it to afford a bigger house than you could with a fixed rate

- You’re risk-averse, and the thought of rising payments would cause you to lose sleep

- Your exit strategy depends on perfect market cooperation and falling rates

- You don’t have substantial emergency funds or flexibility within your budget

- The maximum payment would cause undue financial hardship

Today’s ARMs are less risky than those of the past thanks to better safeguards, but they still require a solid plan and a financial cushion to work in your favor, even if the market doesn’t cooperate.

Talk to a loan officer to see if a 5/1 ARM is right for you

Whether you’re thinking of applying for a mortgage today or in a few months, connecting with a loan officer now can help. An experienced loan officer can look at your current financial profile and advise you on your mortgage options.

At Best Interest Financial, we provide personalized, white-glove service that big-box and automated lenders can’t. With over 80 years of combined experience and billions in closed loans, our loan officers have the expertise to help identify creative financing possibilities that others miss.

No matter what your timeline is, we can help you develop a strategy to reach your goals and get you on the path to home ownership. Get a free, 60-second quote from Best Interest today to learn more.

FAQs

Can rates go down on a 5/1 ARM?

Yes. Your rate during an adjustment moves with its index. Only the lender’s margin remains the same. If the index is down when your rate adjusts, then you could see a lower rate. Your loan’s floor rate may limit how low the interest rate can go.

Can you refinance a 5/1 ARM?

Yes, you can refinance a 5/1 ARM at any point. Common options include a 15- or 30-year conventional loan or another ARM loan.

What is a 5-year ARM interest-only?

A 5-year I-O ARM means that for the first five years of the loan, you pay just the interest portion of your monthly payment. Then you’ll make principal and interest payments for the life of the loan. Longer I-O periods mean higher monthly payments when you make full payments later.

Disclaimer: The information provided in this article is for informational and educational purposes only. It is not intended as legal, financial, investment, or tax advice, and should not be relied upon as such. Mortgage rates, terms, products, and eligibility requirements are subject to change without notice and vary based on individual circumstances, credit profile, property type, loan amount, and other factors. All loans are subject to credit approval. This content does not constitute a commitment to lend or an offer of specific loan terms. For personalized mortgage advice and to discuss loan products that may be suitable for your situation, please contact one of our licensed loan officers.

[/textbox]